Key takeaways

- Net burn — not gross burn — is the number that determines runway; founders who confuse the two routinely overestimate how much time they have.

- Bottom-up revenue forecasting forces you to name a specific number of customers at a specific price — making the forecast falsifiable within 30 days.

- At a 5% monthly churn rate, you lose nearly half your customer base every year; most founders don’t model this compounding effect until it’s already happening.

- A hiring decision, a pricing change, or a single lost anchor customer each warrant an immediate model revision — not a wait until the monthly cycle.

Most bootstrapped founders build a financial model once, feel good about it, and never open it again. Startup booted financial modeling only works if the model is alive: updated monthly, stress-tested quarterly, and connected directly to the decisions you’re about to make.

This guide is built around four moments where your model either saves you or fails you: knowing your real cash position, forecasting revenue without kidding yourself, deciding whether to spend on growth, and knowing when your assumptions have expired.

What Makes Bootstrapped Financial Modeling Different

Bootstrapped financial modeling isn’t a stripped-down version of a VC model. It’s a different tool built for a different job. A VC-backed model is designed to support a story — market size, growth trajectory, path to dominance. A startup booted financial model is designed to answer one question at a time: can we make payroll next month, should we run this ad campaign, does hiring this person extend or shorten our runway?

That means a tighter time horizon (12–18 months, not five years), a higher update frequency (monthly actuals, not quarterly board decks), and a ruthless focus on cash rather than accrued revenue or projected ARR. The biggest mistake is downloading a fundraising template and trying to adapt it. Start with four things: a revenue forecast, a cost tracker, a cash flow view, and a runway number. Everything else is optional until the business demands it.

Getting Your Cash Position Right Before Anything Else

Before you can forecast, you need an accurate baseline. That means knowing your real net burn — not your gross burn.

Gross burn is every dollar leaving your account in a month: payroll, subscriptions, rent, contractors, everything. Net burn is gross burn minus revenue actually received. The gap between the two is where most founders get into trouble. A business bringing in $3,000/month in MRR but spending $7,000 has a net burn of $4,000 — not $7,000 and not $3,000. Runway is calculated on net burn, so getting this wrong compresses or inflates your timeline significantly.

Runway = Cash on hand ÷ Monthly net burn

A worked example:

| Line item | Amount |

| MRR (18 customers × $120/month) | $2,160 |

| COGS (hosting, support tools) | $380 |

| Operating expenses (salary, software, ads) | $3,900 |

| Gross burn | $4,280 |

| Net burn | $2,120/month |

| Cash on hand | $28,000 |

| Runway | 13.2 months |

Track COGS separately from operating expenses. Conflating them hides whether the product itself is profitable — you might be hitting revenue targets while the underlying unit economics are broken.

Break-even deserves a concrete number too, not just a revenue milestone. The formula is Fixed Costs ÷ Gross Margin %. In the example above: $3,900 ÷ (($2,160 − $380) ÷ $2,160) = $3,900 ÷ 82.4% = $4,733/month. At $120 per customer, that’s 40 customers. The business has 18. The gap is 22 customers — a number you can attach a timeline to based on current growth rate.

Forecasting Revenue Without Lying to Yourself

The most common forecasting error in startup booted financial modeling is working top-down: picking a market size, assigning a capture percentage, and calling it a revenue projection. The number feels grounded because it references real data. It isn’t. There’s no operational mechanism connecting “the market is $4 billion” to next month’s invoice total.

Bottom-up forecasting builds revenue from observable inputs: how many active leads you have, what your close rate actually is, what the average deal size has been, and how much capacity you have to close. If you have 25 active prospects, a 15% close rate, and an average first contract of $180/month, your expected new MRR next month is $675. That number can be tested against reality in 30 days. If you miss it, you know exactly which input was wrong — too few leads, a lower close rate, or smaller deals than expected.

For SaaS businesses, model MRR as a running calculation rather than a static projection:

Net new MRR = New MRR + Expansion MRR − Churned MRR

Churn is where most SaaS forecasts quietly fall apart. A 5% monthly churn rate sounds like a minor friction cost. Compounded over 12 months, it means you retain only 54% of the customers you started the year with — a compounding effect that, according to TechCrunch, makes high monthly churn rates effectively unsurvivable for subscription businesses. At 3% monthly churn, that retention climbs to 70%. The difference in runway impact over a year is not marginal — it’s existential at the bootstrapped stage.

Deciding Whether to Spend on Growth

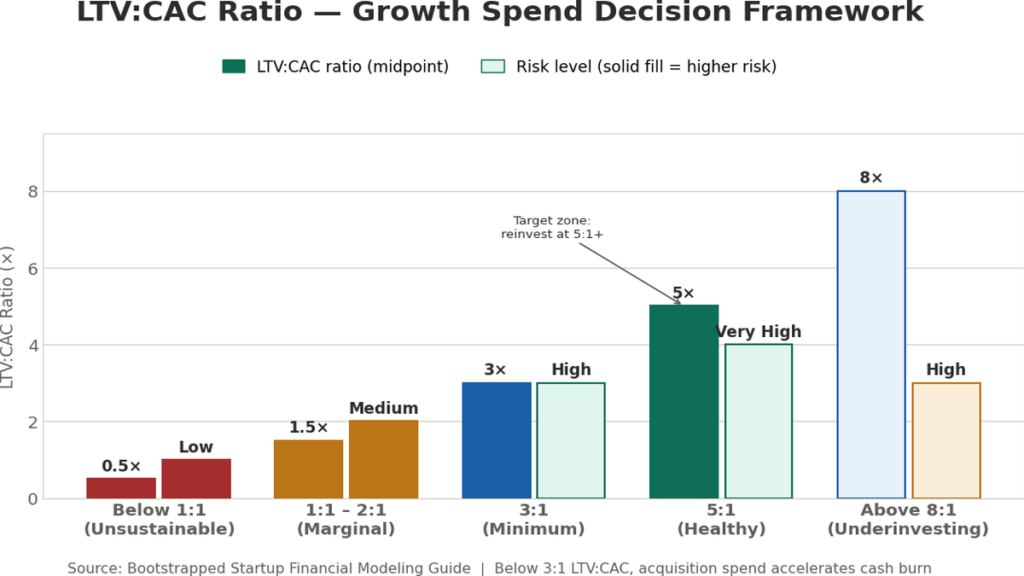

Every bootstrapped founder eventually faces the spend-or-conserve decision: run a new paid channel, hire a first salesperson, invest in a product feature. The model should tell you whether that spend makes sense before you make it.

The unit economics test is the starting point. Calculate CAC (total sales and marketing spend ÷ new customers acquired) and compare it to LTV (ARPU × gross margin % ÷ monthly churn rate). Churn rate — defined by data from Wikipedia as the proportion of customers who leave a group during a specified period — is the denominator that most directly determines how long acquired customers remain profitable. The ratio between LTV and CAC tells you the structural economics of your growth engine:

Below 3:1, growth spending actively accelerates cash consumption without building proportional business value. A bootstrapped founder at 1.5:1 spending $2,000/month on acquisition is spending $2,000 to generate approximately $1,000 in lifetime gross profit.

Knowing When Your Model Has Expired

A financial model built on January assumptions and never touched is not a planning tool by March. The assumptions that felt reasonable at the start of a quarter — churn rate, CAC, conversion rate, average deal size — shift as real data arrives. The model has to shift with them.

Monthly updates should be non-negotiable: log actuals against projections, recalculate net burn and runway, and document the variance. The variance log is more valuable than the projection itself over time — it reveals which assumptions are systematically off and which inputs your business is most sensitive to.

Beyond the monthly cycle, certain events require an immediate model revision regardless of where you are in the month:

- A new full-time hire committed — a single hire can add $5,000–$10,000 to monthly OpEx

- A pricing change — repricing moves MRR, LTV, and break-even simultaneously

- An anchor customer churning — can shift net burn by 30% in a single month

- A meaningful COGS increase — hosting, supplier, or delivery cost changes hit gross margin directly

- Any fundraising conversation — build investor-facing outputs separately from the operational view

Run three scenarios quarterly. The base case reflects your current best estimate. The downside models what happens if your largest assumption is wrong — churn doubles, a major customer leaves. The stretch case tests whether you can handle significant upside without breaking. The downside is the most important: founders who run it regularly report that seeing runway compress to 3–4 months prompts cost decisions the base case never surfaced.

Conclusion

Startup booted financial modeling is not about building a perfect model. It’s about building one you’ll actually maintain — one that reflects what’s true about your business today. Keep it simple enough to update in 90 minutes. Stress-test it quarterly. Revise it immediately when something significant changes. The value isn’t in the projection. It’s in the discipline of watching your assumptions against reality every single month.

Frequently Asked Questions

What is startup booted financial modeling?

Building cash flow, revenue, and expense projections for a self-funded startup to drive operational decisions rather than support investor pitches.

How is it different from a standard startup financial model?

Standard templates optimize for investor optics — market size, growth trajectory, EBITDA. Startup booted modeling optimizes for survival: net burn, runway, and break-even timing updated monthly.

What’s the most important metric to track?

Net burn. It determines runway, and runway determines every other decision. Founders who track only gross burn consistently overestimate how much time they have.

How often should the model be updated?

Monthly at minimum, with immediate revisions after any significant event: a new hire, a pricing change, an anchor customer churning, or a meaningful COGS shift.

When does a bootstrapped startup need a fractional CFO?

When the model stops being updated because it’s too complex to maintain, or when decisions involve multi-entity, multi-currency, or complex revenue recognition. This typically surfaces between $500,000 and $1,000,000 ARR.